Stories

The Quiet Progress of Green Property Funds

Real estate investment management companies are using EDGE for their property funds to show compliance, lower risk and increase profitability and brand value for developers.

Asia Green Real Estate invested in South Quarter, an office complex located in TB Simatupang, the CBD of South Jakarta.

At the nexus between property developers and today’s socially conscious investors stands an increasingly persuasive investment choice. Called a green property fund or impact fund, it’s an influential way for investment managers in emerging markets to match make developers with those who aspire to both profits and positive change.

The concept is simple: fundraise from third party clients to ensure developers in urbanizing markets have the capital to build green. Then keep a tight hold on technical criteria to ensure peak building performance, which will benefit both occupants and the environment, while adding cachet to developers’ brands. It’s a virtuous alternative to building a conventional product and then selling high, with gains mostly derived from improved land value.

The Secret to Green Property Funds

With a property or impact fund, a pool of institutional and private investors combine their capital, then directly or indirectly finance projects. A direct investment could be a joint venture with a developer, and an indirect investment could be an equity stake in shares of a company that develops properties. JVs allow investment managers with green know-how a unique selling proposition, as their competencies aren’t readily available on the market. Investment managers also have quality control of the final product, which narrows project risk.

This formula of the investment manager absorbing the costs of technical oversight through in-house expertise is the secret of success for green funds. There is little additional cost for a green spec when the initial design is adapted to meet requirements, particularly when the investment manager negotiates in bulk with contractors. This keeps the cost of going green negligible.

When it comes time to make a profit, the objective of the fund determines the exit strategy. Income-producing funds might raise capital, build a green field project, and then list the property for ten years. Shorter-term funds might focus on a for-sale product with a higher profit upon exit. The sweet spot is when market prices are increasing due to greater demand than supply, marking the ideal moment for liquidation. Investors can exit and realize their returns, or they might restructure and roll over the equity into a future phase, when new investors are brought in.

A Shared Belief in Resource Efficiency

According to Asia-based investment company Asia Green Real Estate with offices in Jakarta and Shanghai, there is a link between real estate returns and GDP growth. With the balance of macro-economic power shifting from the West to the East, that pushes Swiss pension fund investors to think outside their own country, which is currently experiencing negative interest rates.

Alex Buechi, a partner and head of ASEAN Markets for Asia Green Real Estate, is ready to meet his investors’ needs with carefully vetted projects from Indonesian developers who share his belief in the profitability of resource-efficient buildings.

“Once we have understood the developer’s intention, it’s like a marriage,” said Alex. “Even though the developer can get financing elsewhere, there’s loyalty, as we share the same mindset. We both understand that green must be intrinsic and not a gimmick. In turn it is understood that my firm won’t compete with the developer through overlapping activities.”

Less Headaches, Higher Rewards

Green property funds have existed for less than a dozen years and there is little empirical evidence of strong capital gains, particularly when firms are quiet about their success. However internal returns of between 20 to 30 percent are not uncommon, proving that difficult markets can be resilient and reap high rewards.

While often perceived from outsiders as risky, increasing land value in emerging markets makes property investments relatively safe as the underlying asset is the acquired land. Complexities such as the percent of ownership allowed by foreigners or land ownership eventually reverting back to the government are handled by the investment manager, ensuring investors don’t take on headaches they can’t handle.

Voices from Africa

One of the most difficult markets is commodity-dependent West Africa, where RMB Westport was created in response to the shortage of A-grade assets. The firm is a hybrid between an equity financier and an experienced developer, born from the realization that the best model for challenging markets is to combine balance sheet skills with local development expertise.

“The process is a big part of the risk,” said Alan Wilson, CFO of RMB Westport. “Being directly involved with our hands firmly on the wheel is a key factor in how we deliver good returns on our properties in difficult markets. That’s how we control quality, lower the risk profile, and help to solve the demand and supply mismatch.”

International Housing Solutions (IHS) invested in Clubview Residential Development outside of Johannesburg, which include smart meters for energy and water efficiency.

What is most important to socially conscious investment fund managers is absolute certainty that the project benefits the end user, who is often the low-to-middle income homeowner. Willem Odendaal, a technical specialist at South Africa’s International Housing Solutions who lives by the credo “you can’t manage what you can’t measure,” has installed smart meters in affordable green homes to monitor electricity and water consumption, and provides education to tenants to ensure performance as projected.

IHS is also undertaking a test by pitting a 200-unit green development against a similarly-sized non-green development next door. Positive results from the test will prove to the banking industry that green mortgages should be offered to qualifying homeowners. IHS plans to build 14,000 rentals and 6,000 for-sale units in the near future, all of them affordable and with resource-efficient design.

South Africa’s Old Mutual Alternative Investments (OMAI), with US$4 billion in assets under management and ambitions to expand elsewhere in Africa, takes a head-and-heart approach through funds that combine bottom line returns with a development agenda. They are passionate about “non-obvious” opportunities where there is a serious gap in social infrastructure, such as affordable housing and quality schools.

“More and more investment firms are being held accountable,” said Lenore Cairncross, an Investment Professional for Development Impact Funds at OMAI. “Their clients want to know if their money is positively impacting society as a whole. When they look at competing investments, which will they choose? If the returns are close, they’ll choose the sustainable one.”

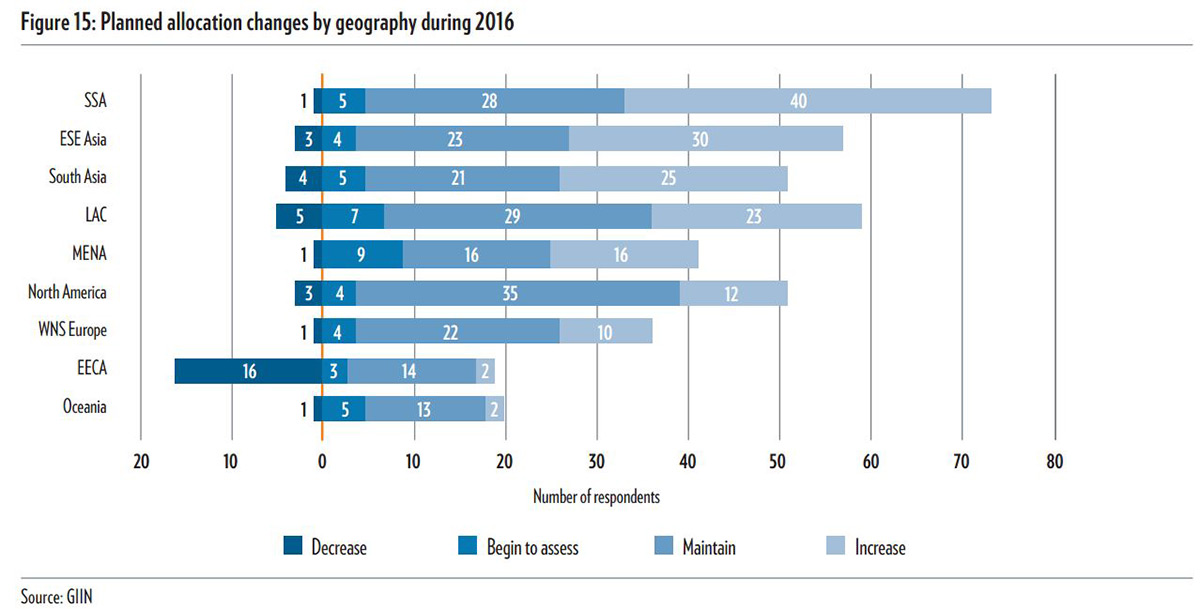

Global Impact Investing Network’s Annual Impact Investor Survey 2016 indicates that emerging markets will become an area of focus for impact investors, particularly in Sub-Saharan Africa.

A Bright Future for Green Funds

According to Alex Buechi, the fact that Swiss high-net individuals and pension fund managers enjoy the impact of their Asian green building investments shows promise for the space to become more crowded in the future. With increased regulatory pressures and gains in market sophistication, the field of socially responsible development is bound to attract more attention.

“I hope there will be more competition in our fund environment,” said Alex. “Where there is no competition there is no market. It’s about innovation at the end of the day. And we will never stop reinventing ourselves.”

“The Quiet Progress of Green Property Funds” originally appeared in The Triple Pundit and has been published with permission.